Uncommon Sense

July 2026 Newsletter

Well, what a strange few weeks of weather we’ve been having. Blazing heat one minute, weeks of rain the next. Good luck being a farmer trying to plan around that.

Meanwhile, there’s plenty to keep us distracted. Wimbledon is underway, the strawberries are out, and the football World Cup is in full swing. If you’re anything like me, the evenings have taken on a certain nervous energy. Supporting England has never been the most relaxing pastime, but there’s something rather nice about a tournament that has the whole country holding its breath at once. However it’s all unfolding by the time you read this, it’s a welcome distraction.

The rest of this month’s newsletter is packed with ideas and links that you may find interesting. As always, we’re here if you’d like to discuss how any of these ideas might apply to your unique situation.

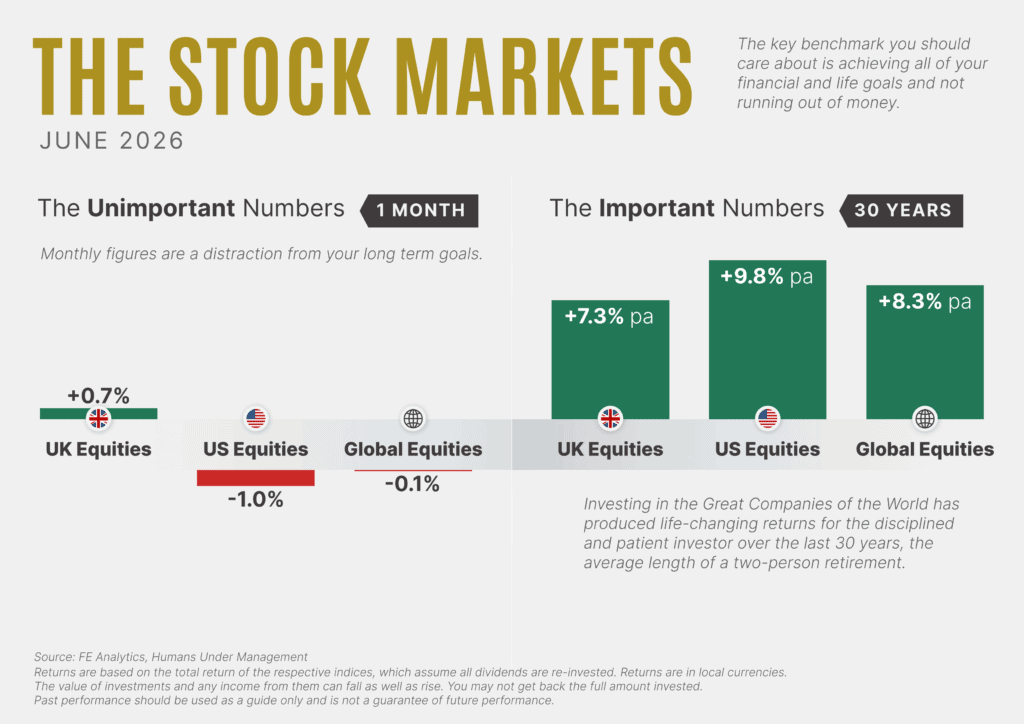

The Stock Markets

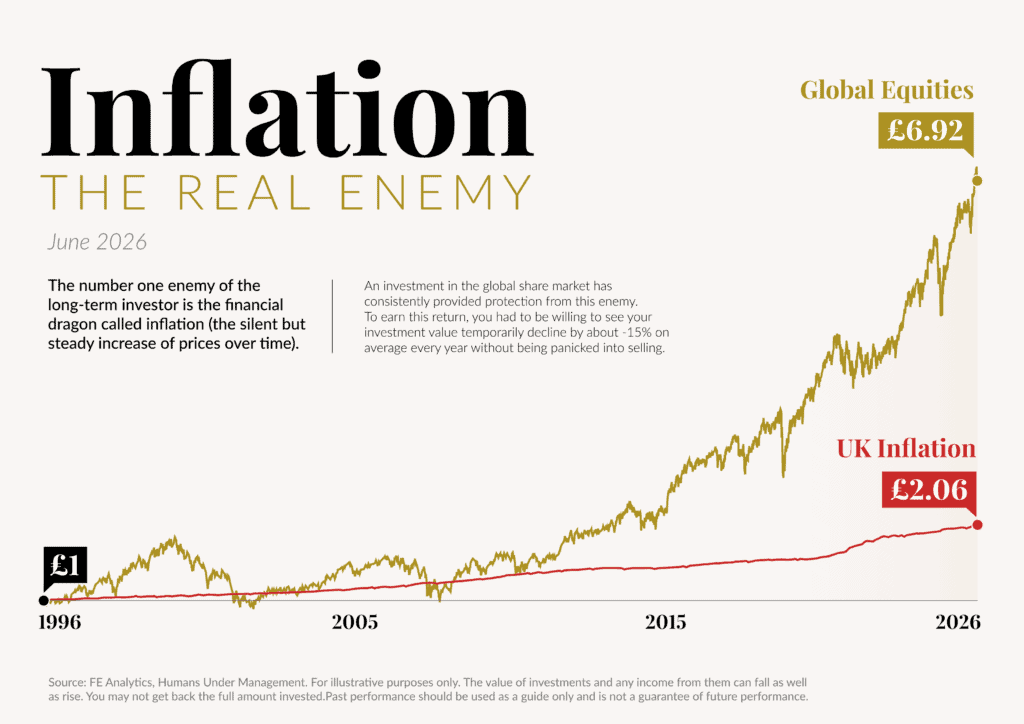

Inflation – The Real Enemy

📰 Read

A Sunday Thought About Money [2 minutes]. What all the saving is really for.

Why Your Financial Plan Is Already Wrong [3 minutes]. Why your plan was wrong from day one, and why that’s fine.

The Dangerous Allure of “Dying with Zero” [5 minutes]. A hospice doctor’s counterweight to “die with zero.”

Anniversaries [1 minute]. Why an anniversary is a decision, not a date.

Behavioural Lessons From the World Cup [2 minutes]. The biases that trip up investors, spotted on the pitch.

Is Life Worse Today Compared to 10 Years Ago? [6 minutes]. Three biases that make the present feel worse.

🍿 Watch

🎧 Listen

Look Where You Want to Go [5 minutes]. Focusing on the obstacle often pulls you toward it, while looking beyond it helps you move through it.

😀 Rational Optimism

The media is not a friend of the disciplined and patient investor. Ignoring the key determinants of lifetime investor returns, the media focuses on short-term returns, market predictions, and negative news.

We present the following as an antidote to the onslaught of negative news:

Data Show Freeing Economies Doesn’t Harm the Environment

The Western World’s First Grid-Scale Small Modular Reactor

A Growing African Middle Class Is Increasingly Mobile

🖼️ A Picture is Worth a Thousand Words

How the World Added Decades to Life Expectancy

The Biggest IPOs in History—and Where SpaceX Fits In

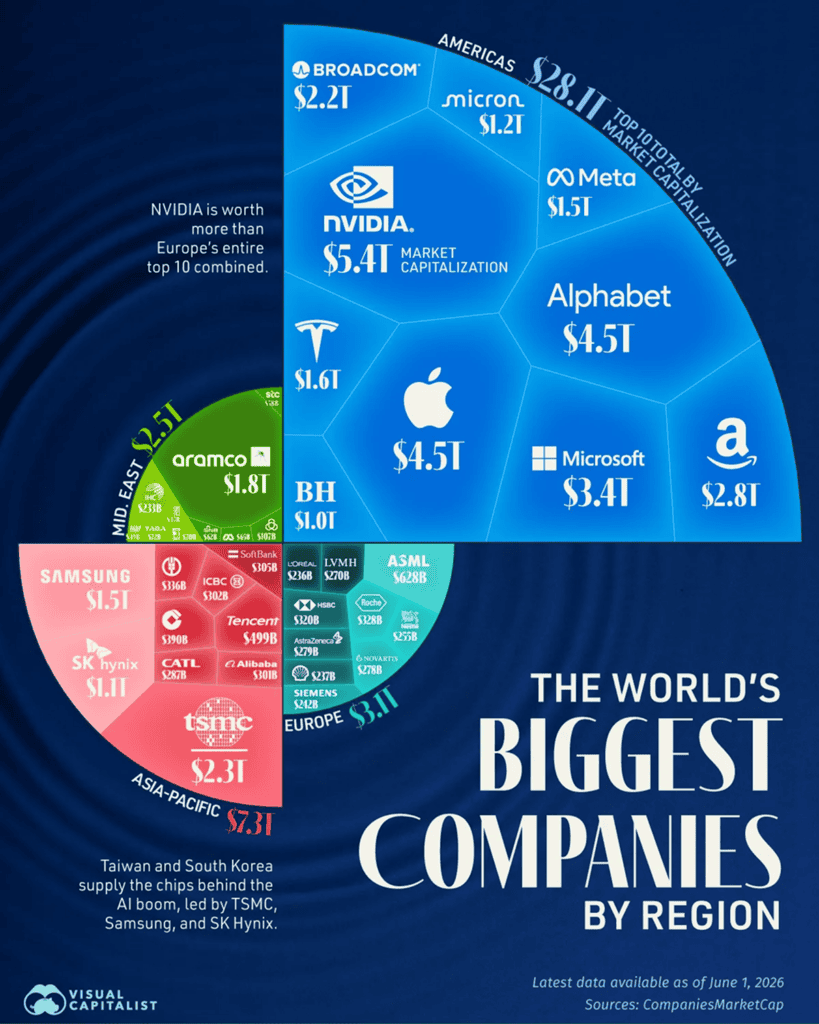

The World’s Biggest Companies by Region

2026 Midyear Review

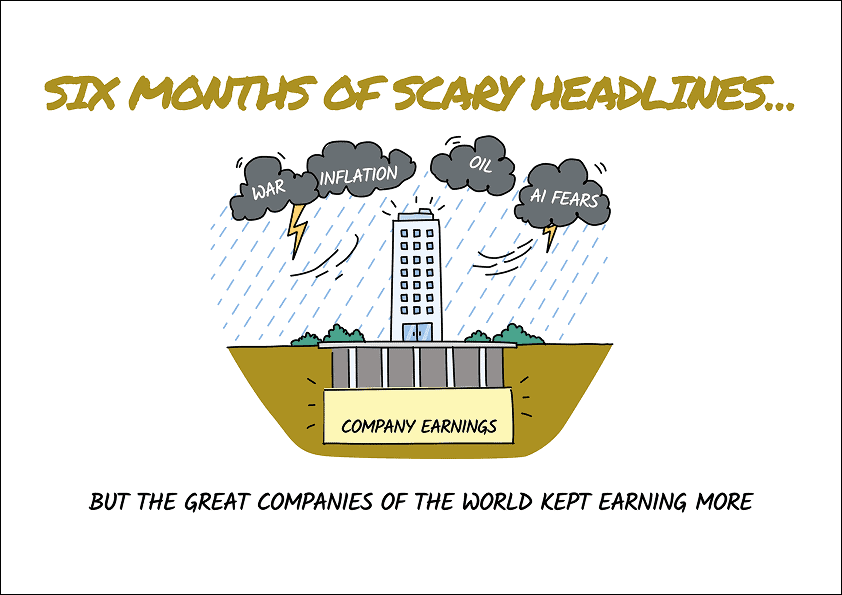

The halfway mark of the year is a good place to stop and look back. Six months of news tends to blur together, and the point of a review is to separate what actually mattered from what only felt urgent at the time.

At the start of the year, we cautioned that after three strong years for global markets, a temporary market decline would not be unusual, that any setback would probably be set off by something few of us were discussing, and that the one risk worth watching was how heavily the market leaned on a small group of large technology companies to continue to grow their earnings.

What’s Happened

A small setback and decline did arrive, but not from the direction many expected.

The Strait of Hormuz

In late February, the United States and Israel launched military strikes against Iran. The Strait of Hormuz was closed, disrupting a large share of the world’s oil supply, and the price of oil doubled within weeks. Inflation, which had been easing, began to climb again, and markets fell and swung sharply through March and April.

A conditional ceasefire and framework have since been reached, and oil has fallen to a level slightly higher than it was at the beginning of the year.

Market Returns & Inflation Concerns

We started the year expecting further interest rate cuts, but due to the conflict’s inflationary effects, the next interest rate change is now more likely to be upwards than downwards.

Although markets declined during the peak of uncertainty, they did not crash. By mid-2026, both the US and global markets have increased by approximately 9 percent. The specific value in your currency will vary based on exchange rate fluctuations during this time.

The reason for that resilience was not market sentiment but real corporate earnings. Through the first quarter, the world’s major companies extended a run of strong profits into a sixth straight quarter, and full-year estimates have since been revised upwards.

SpaceX IPO

The last notable event was the SpaceX initial public offering (IPO), the largest of all time. With a few other large private companies expected to list soon, the major market indices will soon include companies that have until now been available only to a select group of private investors.

What we’ve Learned

The first half of the year offered three lessons worth holding onto.

The trigger is rarely the one you are watching.

In January, the risk on most minds was the technology sector and the chance its spending would disappoint. The actual shock was a war. The risks everyone can see are mostly already reflected in prices, so the ones that move markets are the ones not being discussed. You cannot prepare for a surprise you have not imagined. You can only build a plan that does not depend on knowing what comes next, with enough money set aside to cover near-term needs.

A frightening half-year can still be a profitable one.

It would have been easy in March to sell and step aside until things calmed down. Anyone who did would have locked in losses near the low and missed the recovery. The tariff scare of April 2025 taught the same lesson. The discomfort of staying invested through a decline is real, but it’s the price of admission for long-term investors. Bad news and a rising portfolio sit together more often than most people expect.

The risk we named arrived, and a diversified portfolio absorbed it.

For two years, the common worry was the market’s reliance on a handful of giant technology companies, and the fear that if they stumbled, they would take the whole market down. In the first half of the year, these companies (often called the Magnificent Seven) underperformed the overall market. The risk was not resolved in the crash many investors feared, but in a rotation to the broader market. The rest of the market rose to meet the gap, once again proving why diversification matters.

Looking Ahead

The second half of the year will bring its own surprises, as every period does. Inflation has not fully settled, interest rates may rise rather than fall, and the peace in the Middle East is recent and untested.

There will be worries we are not yet naming, and at some point, there will be another decline. This is a normal, recurring part of investing rather than a sign that something has broken down.

Three good years did not entitle us to a fourth without interruption, and the first half delivered the kind of interruption we expected, even if the cause was one we did not expect.

As ever, it is a privilege to help you navigate these years. If you would like to discuss how recent developments affect your own financial life plan, please let us know.

Compliance Disclaimers:

The value of investments and any income from them can fall as well as rise. You may not get back the full amount invested. Past performance should be used as a guide only and is not a guarantee of future performance.

We hope that you enjoyed this month’s newsletter. Please let us know what you enjoyed, or write back with any of your own news.

As always, we’re here for you.

See you next month,

Halcyon Financial Planning

![]()