Uncommon Sense

February 2026 Newsletter

After easing into 2026, the year already seems to be moving at full speed. The financial media has wasted no time latching onto its favourite themes. While these topics generate plenty of noise, they rarely deserve the attention they receive when viewed through the lens of a long-term financial plan.

In this month’s newsletter, we explore what we call the “10-year test”, a simple but powerful way to evaluate whether today’s headlines truly matter to your financial future. We hope it helps put the current noise into perspective

The rest of this month’s newsletter is packed with ideas and links that you may find interesting. As always, we’re here if you’d like to discuss how any of these ideas might apply to your unique situation.

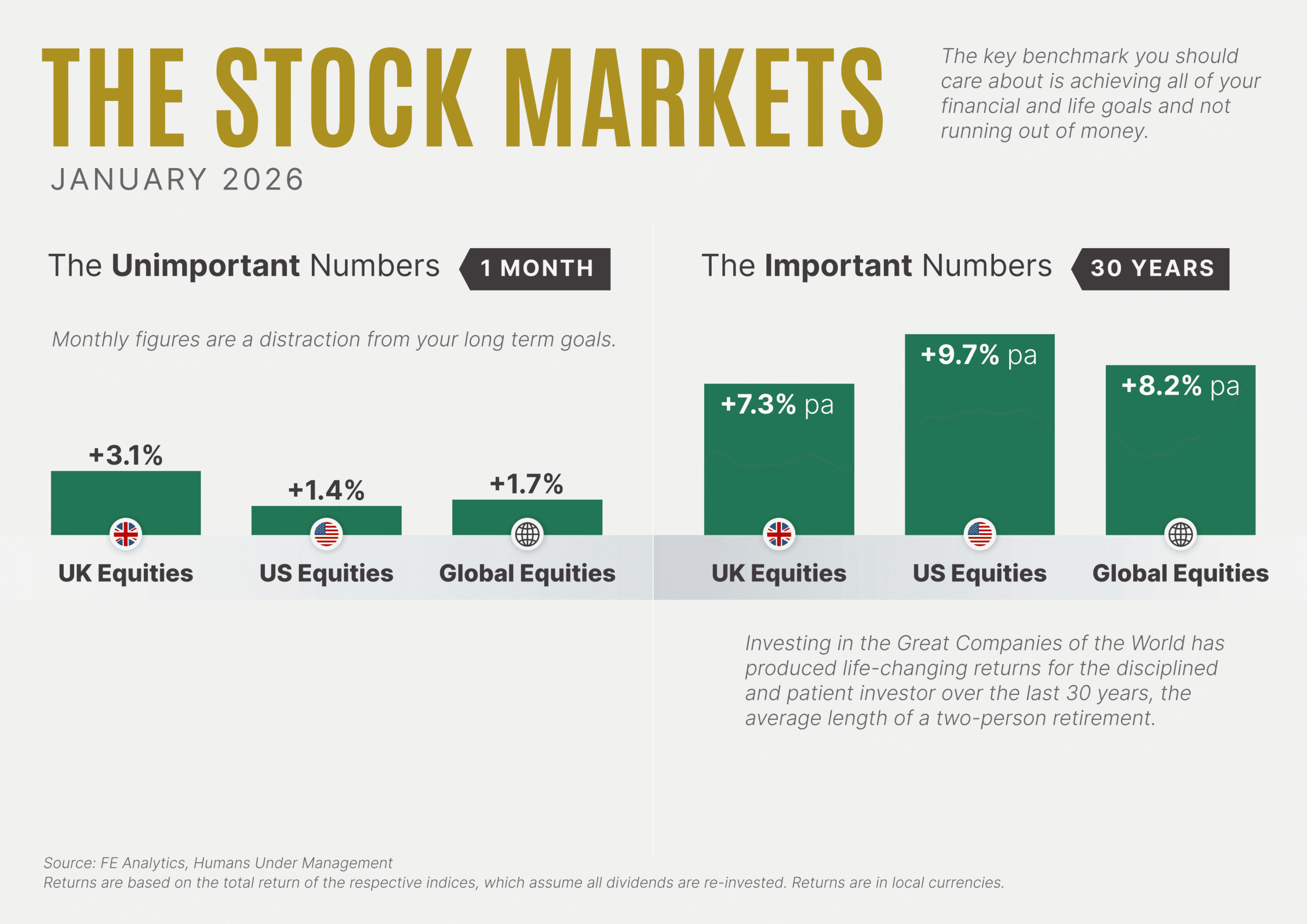

The Stock Markets

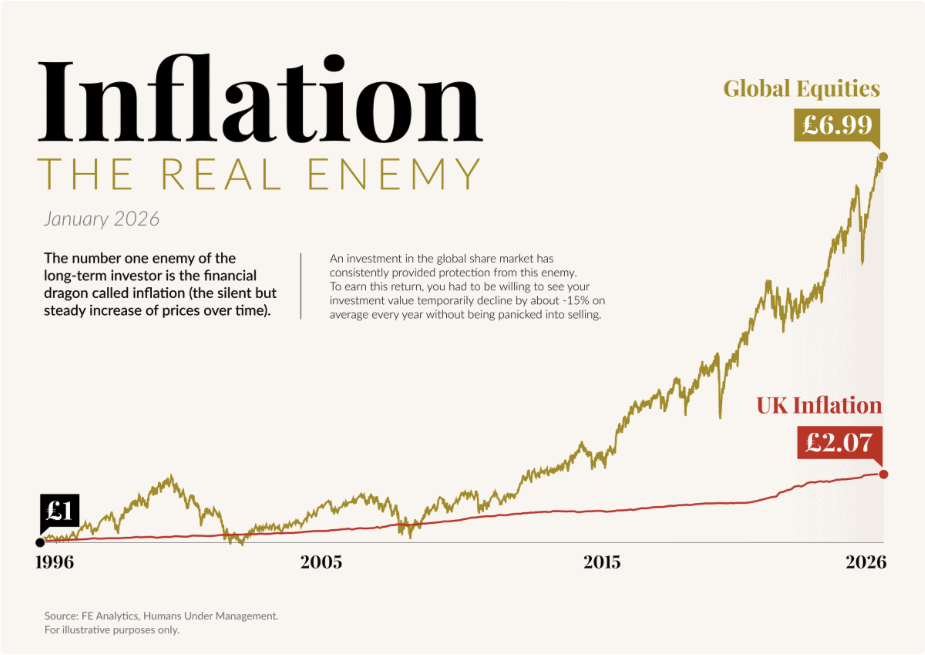

Inflation – The Real Enemy

📰 Read

The Gifts We Give Our Kids [10 minutes]. Explore how the gifts we give our kids can shape their character and financial future in ways that money alone cannot buy.

An Antidote to “Personal Stagflation” [9 minutes]. Explore how embracing small joys and hobbies can be the antidote to your personal stagnation and lead to a richer, more fulfilling life.

Out of Control [4 minutes]. What if our biggest worries are out of our control, and focusing on them costs us the present moment?

A Few Things I’m Pretty Sure About [6 minutes]. What if the very challenges we face today could pave the way for a brighter future?

We Need to Talk About Your Retirement ‘Spending’ [7 minutes]. Uncover how thoughtful spending can enhance your life and those of your loved ones.

What does it actually mean to live a good life? [7 minutes]. How can we cultivate lasting happiness beyond fleeting moments of pleasure?

🍿 Watch

3 lessons on decision-making from a poker champion

🖼️ A Picture is Worth a Thousand Words

The Busiest Domestic Flight Route in Every Region

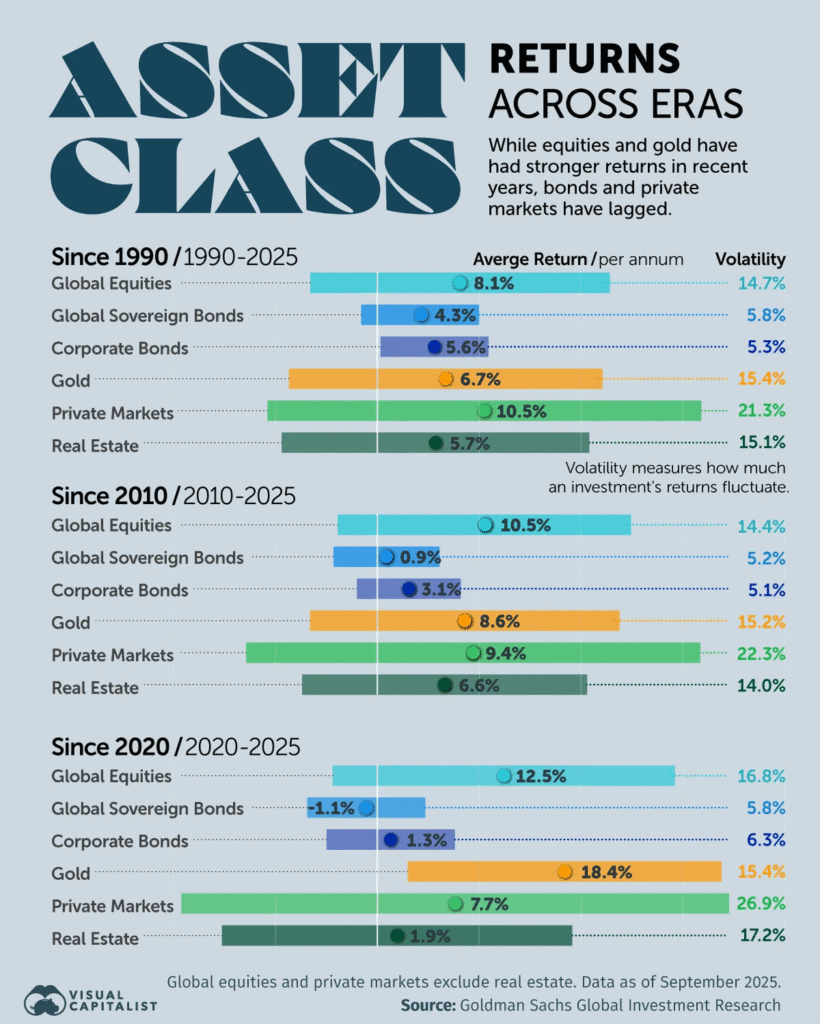

Asset Class Returns Across Eras (1990–2025)

🎧 Listen

What a Plan Actually Is… [8 minutes]. What if planning isn’t just a static document but a dynamic practice that evolves with your needs?

😃 Rational Optimism

The media is not a friend of the disciplined and patient investor. Ignoring the key determinants of lifetime investor returns, the media focuses on short-term returns, market predictions, and negative news.

We present the following as an antidote to the onslaught of negative news:

Food Supplies Everywhere Have Grown Faster than the Population

UK to Extend Life of Sizewell B Nuclear Plant by 20 Years

GLP-1 Adoption Is Changing Consumer Food Demand

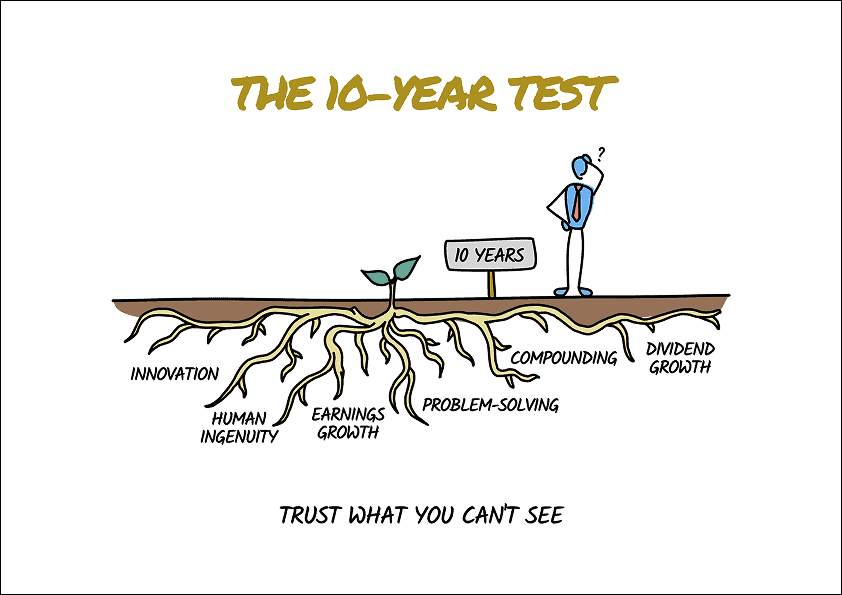

The 10-Year Test

You’ve done the hard work of creating a workable financial life plan that accounts for your current circumstances and future goals. You’ve implemented it using evidence-based, well-diversified investment portfolios. Now imagine you cannot touch any of it for 10 years. No checking. No adjusting. No reacting to whatever headlines appear along the way.

For most people, this idea feels uncomfortable. Maybe even reckless. Surely good investing requires attention, vigilance, and regular fine-tuning?

Before you panic, we’re not suggesting you literally do this. But adopting the spirit of that approach would leave most investors significantly better off. This simple thought experiment tells us something important about where investment success really comes from.

What the 10-Year Test Actually Measures

The test is not whether your investment will rise every year. History teaches us that it won’t. We know that markets don’t move in straight lines. Temporary declines are not a flaw in the system; they are part of the journey.

The real test is whether you can stay invested when things feel uncomfortable.

This is where most investors get it wrong. They don’t fail because they made bad decisions. They fail because they abandoned good decisions at the wrong time. They sold during a decline that proved temporary. They switched strategies just before the old one started working. But mostly, they fail because they let short-term discomfort override long-term logic.

Simply put, the 10-year test separates investors who reach their goals from those who don’t, not because of what they knew, but because of how they behaved.

Why We Feel the Need to Act

Investment growth happens slowly and subtly. There is no daily progress report, no clear signal that things are working. And if you wanted to see daily progress, you wouldn’t find it by checking stock prices. You’d find it by walking the floors and offices of the great companies of the world, watching innovation and problem-solving in action.

But we can’t walk those floors. So we check prices instead. We tinker. We react to headlines. We convince ourselves that doing something is better than doing nothing.

Unfortunately, interfering with a long-term investment not only fails to help; it actively damages the outcome. Every unnecessary change interrupts the compounding process. Every emotional reaction risks locking in a loss that could have been recovered from. Every attempt to “improve” based on recent news pulls you further from your original plan.

Charlie Munger, Warren Buffett’s long-time partner, put it best: “The first rule of compounding: Never interrupt it unnecessarily.”

Most of the damage we see doesn’t come from bad investments. It comes from good investments that weren’t given enough time.

What ‘Doing Nothing’ Really Means

Discipline is not the same as neglect. Doing nothing doesn’t mean ignoring your finances. It doesn’t mean never reviewing your plan or pretending markets don’t exist. It means avoiding emotional reactions. It means trusting a strategy that was built for the long term.

A good plan is personal to you. And a good portfolio isn’t one that goes up every year. It’s one you can stick with through all market cycles. Your plan was designed with this in mind. It expects uncomfortable periods. When the markets fall or headlines turn grim, the plan doesn’t need to change. Your behaviour needs to match it.

Being disciplined and patient is an active decision to stay the course when everything around you suggests otherwise.

Sometimes, the most valuable thing we can do is help you know what not to do. If the 10-Year Test feels uncomfortable, that’s worth exploring together. We’re here to help.

We hope that you enjoyed this month’s newsletter. Please let us know what you enjoyed, or write back with any of your own news.

As always, we’re here for you.

See you next month,

Halcyon Financial Planning